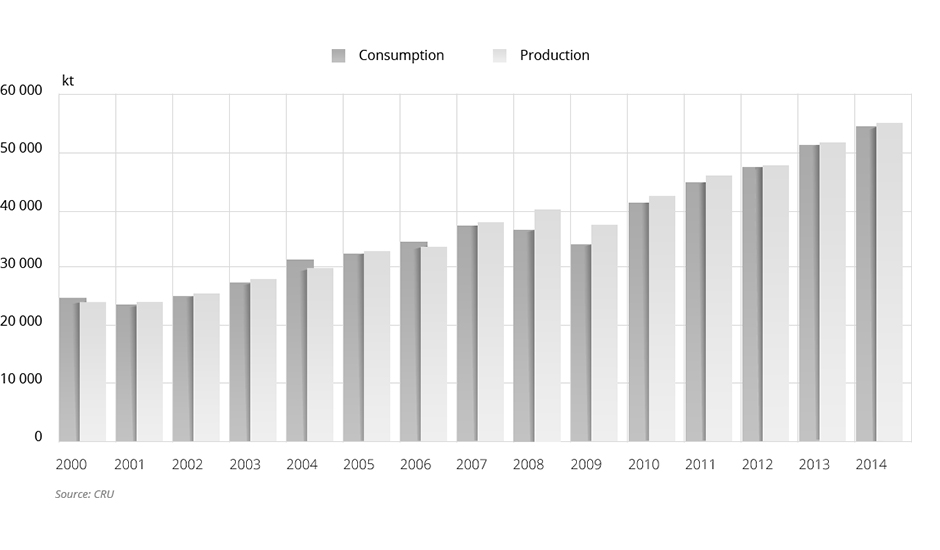

The constant upward trend is accounted for by the fact that aluminium is the metal of progress. State-of-the-art developments in the motor industry, construction, electric engineering, aircraft industry and creation of new gadgets all involve the application of aluminium. This metal enables both the engineers and the designers to solve their problems.

At the same time the increase in aluminium consumption takes place against the backdrop of growing global urbanisation and industrialisation. And while the developed countries have reached a high point in their economic development, the developing countries continue to grow aggressively.

The global aluminium market today can be conventionally divided into two parts: China and the rest of the world. During the last decade, China showed remarkable rates of economic growth including becoming the world's largest aluminium producer and consumer.